The photonics industry can thrive in the UK – but we must be decisive and act fast, say industry leaders.

Photonics is not a single product or industry. It is concerned with how light is generated, transmitted, detected, and manipulated. Photonics technology is found inside many electronic devices, such as fibre broadband cables, MRI scanners, LiDAR sensors, and cancer-detecting imaging systems, to name but a few. And now, it is increasingly being used in the creation of the chips that link together the processors powering AI data centres.

In 2022, the global photonics market reached an estimated $666 billion. A figure that is forecast to move beyond the $1 trillion mark by 2031.

So, where is the UK on this $1 trillion journey? According to a recent TechUK industry briefing, the UK is a research powerhouse, and though it has the potential to be great, it has not fully capitalised on what it has … but it needs to, and fast.

The photonics report

Over six months, techUK brought together companies, researchers, government officials, and sector bodies, and, through research, roundtables, panel discussions, and written submissions, the ‘Photonics: A Vision for UK Leadership in Light-Based Technologies‘ report was born. In February 2026, the Council for Science and Technology (CST) wrote to out-going UK Prime Minister, Sir Keir Starmer, and set out the case for photonics as a strategic national priority, citing that by 2035, more than 60% of the UK economy will directly depend on photonics to ensure the UK remains competitive.

In its letter, the CST described how photonics is foundational to AI, quantum technologies, advanced manufacturing, telecommunications, and healthcare. It stated that the UK’s opportunity is real, but it has a short window of opportunity, and that competitor nations such as the US, China, and Taiwan are already investing heavily and moving fast.

The techUK report builds on that assessment, arguing that photonics is now coming to the fore. It is moving into an indispensable technology and should now be a mainstream policy conversation.

The UK: strong on science, slower to scale

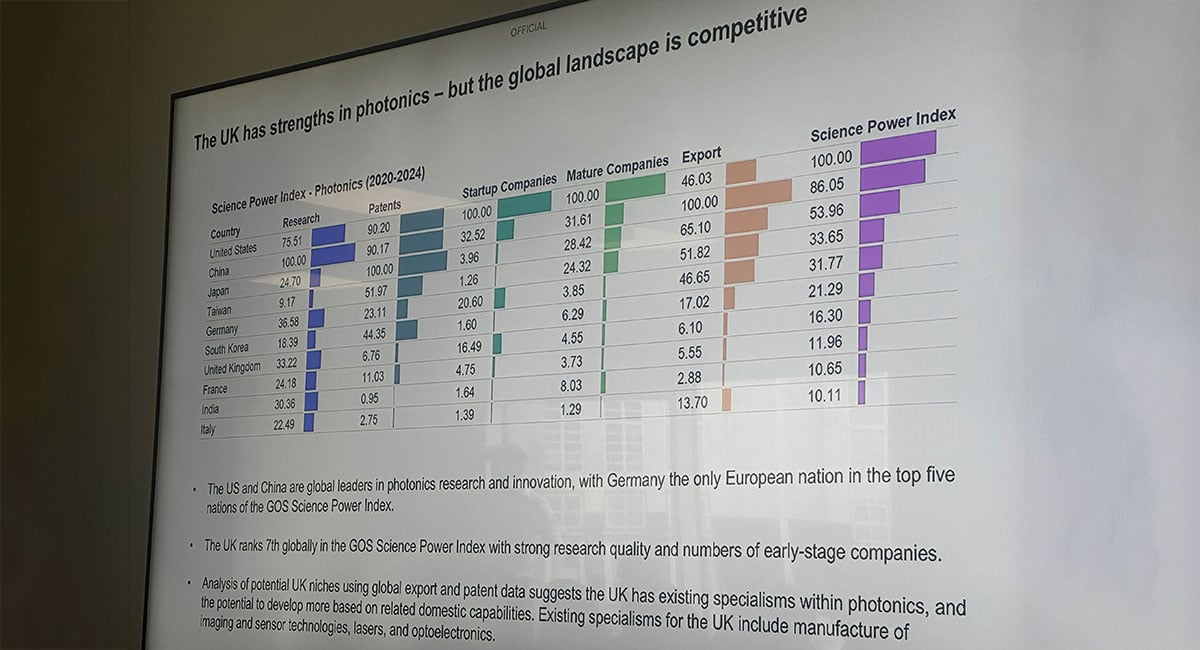

Opening the discussions at the techUK headquarters in June 2026, Rory Daniels, Head of Emerging Tech at techUK, said that the UK photonics sector currently generates approximately £68.6 billion in economic value and employs around 84,000 people.

According to the Science Power Index, the UK ranks seventh globally overall but first in research quality. The UK also has a wealth of cluster expertise developing in areas such as Southampton, Cambridge, Sheffield, Strathclyde, and Belfast.

The problem, according to the techUK report, is that the UK has consistently struggled to translate its research expertise into companies that scale and export. It is great at producing strong early-stage startups, but it consistently falls well behind the US (where many UK startups migrate to). Although, one might have to look at the relative proportional sizes of each country to further quantify the numbers.

Daniels said: “Science has never really been the problem with photonics. The UK is brilliant at the science, and it always has been. The hard part has always been everything that comes after the science – scaling the funding, the factories, the coordination.”

Why do photonic integrated circuits matter?

Joe Gannicliffe, Head of Photonics at CSA Catapult, said that the scale of AI data centres has grown from around 10,000 connected GPUs in 2022 to hundreds of thousands today. They are reaching their physical limits – they produce heat, consume power, and cannot keep pace with the data volumes being generated. Photonic interconnects, which transmit data at the speed of light, are already being deployed, and their adoption is accelerating.

“Photonics is not just an enabling capability within AI hardware and AI infrastructure,” Gannicliffe said. “It’s actually the critical dependency. These hyperscalers are not going to be able to scale without photonics.”

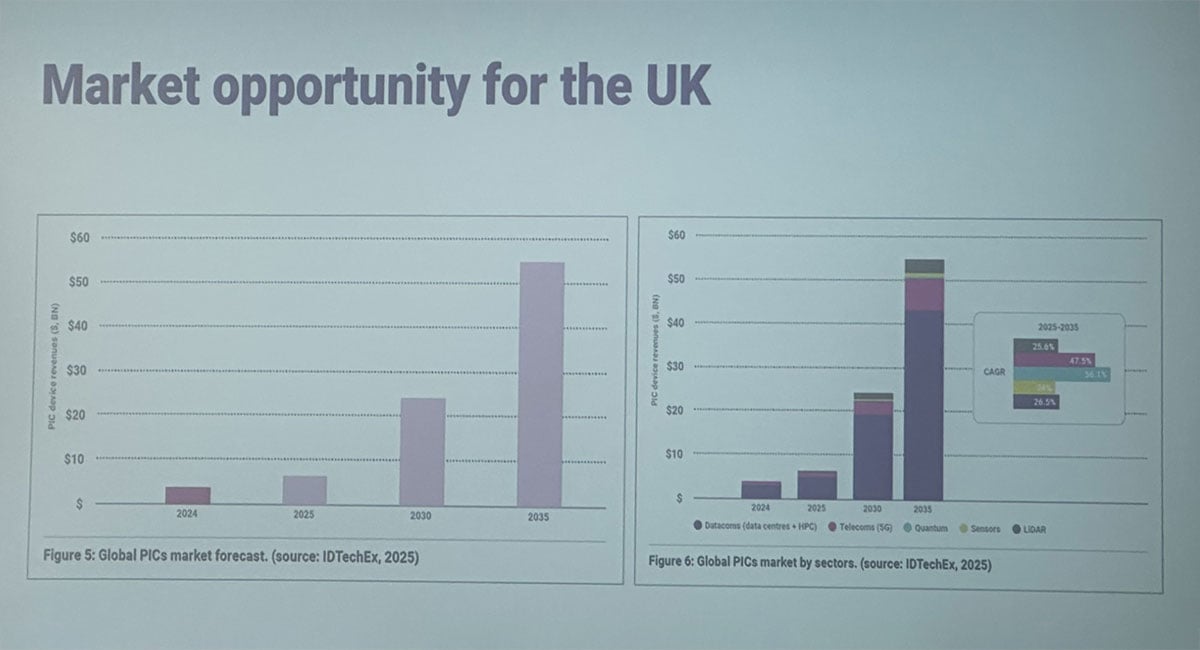

The silicon photonics market is projected to grow from around $4 billion in 2024 to $50 billion by 2035, said Gannicliffe. And quantum computing, which also depends heavily on photonic components, is expected to be the fastest-growing segment within that period.

The five barriers to turning potential into reality

The techUK report has identified five key areas that are preventing the UK from converting its research and industrial capabilities into sustained commercial leadership.

Visibility

Photonics sits across multiple sectors and multiple government departments, meaning it often falls between policy priorities.

Fragmentation

The UK has multiple strong regional clusters, but there is limited coordination between them. This runs the risk of clusters replicating each other’s capabilities rather than building on each other’s strengths.

Skills

Skills shortages are recognised as the second biggest barrier to growth in the sector, behind funding.

Investment

Developing and commercialising a new photonic component or system can take 10 to 15 years. Most venture capital and much public funding are structured around shorter return periods, which means companies often face gaps in support at the critical point between early-stage proof of concept and viable commercial product.

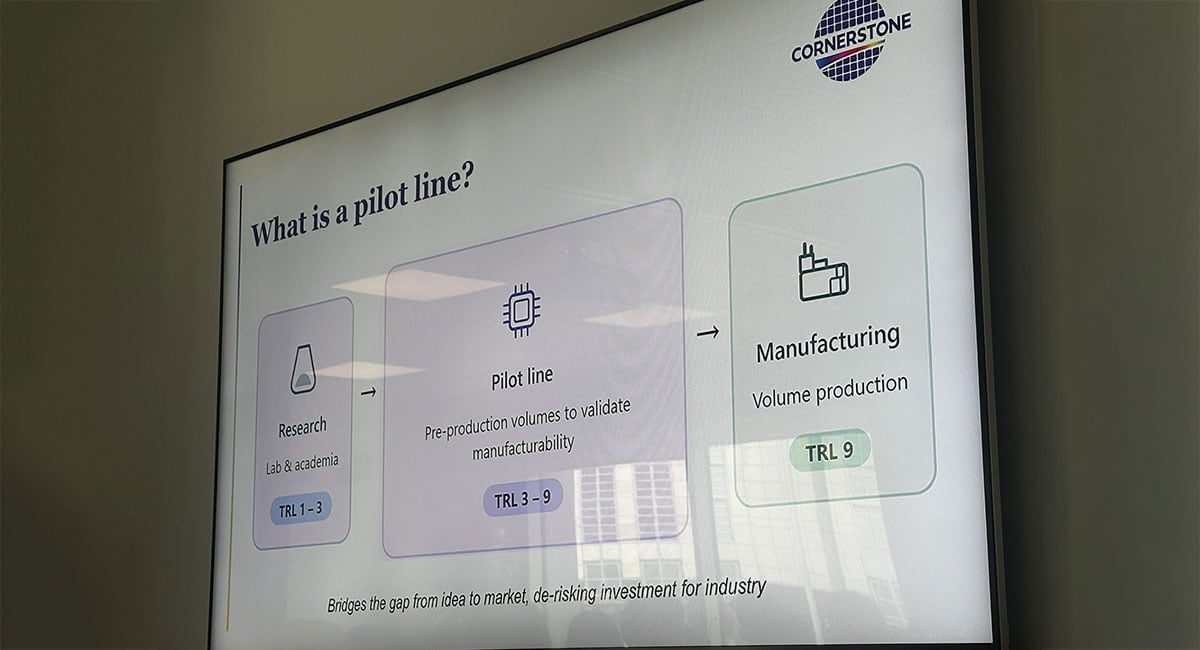

The prototype and production gap

The UK has world-class laboratory fabrication. What it lacks are the facilities capable of producing photonic chips in volumes large enough to validate that a product can be manufactured consistently and at scale, without requiring a company to commit to the costs of full industrial production.

techUK’s eight recommendations

The techUK report sets out eight recommendations on how to move forward.

Publish a National Photonics Roadmap

The UK does not currently have a dedicated national strategy for photonics, while the US, Germany, and the EU all have established frameworks. A roadmap, co-designed with industry, would provide the long-term visibility that companies need to plan investment and recruitment. However, the roadmap must be clear with milestones and deadlines, not aspirational language.

Enhance mapping of the UK’s photonics clusters

The report calls for an improvement to the Department for Science, Innovation and Technology’s (DSIT) Innovation Clusters Map for photonics, to ensure the full geographic reach of the sector is accurately represented and to support better-targeted investment and policy decisions.

Develop a dedicated photonics skills strategy

The report calls for a strategy that treats the sector on its own terms – covering apprenticeships, degree-level programmes, retraining routes from adjacent disciplines, and early-stage school engagement to build the longer-term pipeline.

Build funding models suited to hardware development timescales

The report calls for patient capital structures designed around the 10-to-15-year development cycles that photonics and other hardware technologies require.

Use public procurement strategically

The report recommends coordinating demand signals across departments and creating faster procurement routes, with the aim of generating stable market conditions that can reduce the risk for private investors.

Commission a taskforce to develop a business case for a UK pilot line

A pilot line is a semi-industrial fabrication facility capable of producing photonic chips at volumes sufficient to prove that a product can be manufactured consistently – bridging the space between university research and full commercial production.

Empower the UK Semiconductor Centre to help coordinate the photonics ecosystem

The report argues for the semiconductor and photonics sectors to be more deliberately connected, given the technological overlap between them – particularly in silicon photonics – and to reduce competition between overlapping initiatives.

Tie photonics explicitly into the UK’s broader industrial strategy

Given that photonics underpins quantum, AI hardware, telecommunications, and defence, the report argues for photonics to be named and resourced within national strategies for those sectors, rather than remaining implicit.

The Pilot Line

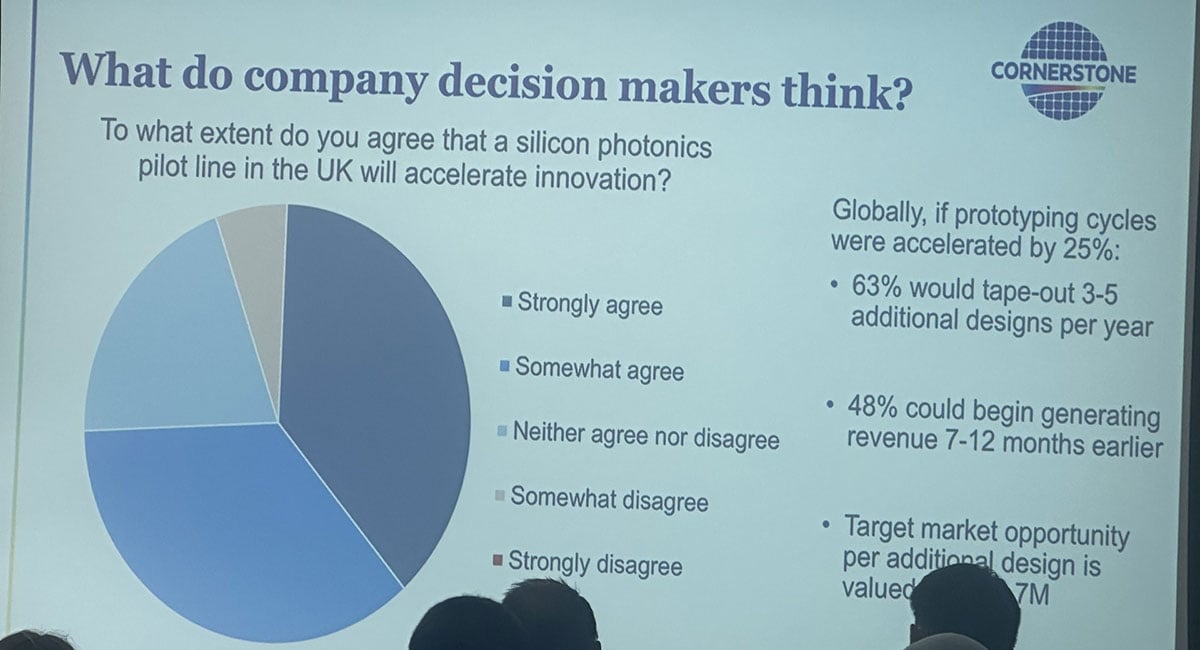

Callum Littlejohns, Deputy Director of CORNERSTONE at the University of Southampton, presented survey results from 500 decision-makers at companies either deploying silicon photonics or planning to do so within two years. Responses came from five countries, including 100 UK companies.

The results found that around 87% of UK respondents said a dedicated fabrication facility would help them scale. Three-quarters agreed that a pilot line would accelerate their innovation. Of those surveyed globally, 63% said that a 25% reduction in their prototyping timeline would lead them to introduce three to five additional products per year. Almost half said they would begin generating revenue seven to 12 months earlier than would otherwise be the case.

CORNERSTONE’s proposal calls for a facility covering multiple material platforms – including silicon nitride and lithium niobate alongside standard silicon – and offering fabrication, integration, packaging, and testing under one roof. An independent economic assessment estimates that a capital investment of around £300 million in such a facility would generate approximately £3 billion in gross value added for the UK economy by 2040 and support around 3,000 additional jobs among the companies using it.

However, this is not as a given, but as a case being made: “We just need someone to stand and back it,” said Littlejohns.

The US, China, Taiwan, and Singapore have identified photonics as a strategic technology and are committing national resources to it. The UK’s window to establish a position that competitors cannot easily displace is estimated by the CST to be three to five years.

Coordination challenge

It is believed that the UK’s problem is that “the sector’s biggest threat quietly shifts from neglect to miscoordination,” said Daniels.

Elizabeth Patterson, Senior Policy Programme Manager at Seagate in Northern Ireland, said: “It’s clear where we are strong … We know we’ve got great skills in Southampton and Cambridge. We know we’ve got great manufacturing in Northern Ireland. We know we’ve got advanced packaging in Scotland. It’s not an area we need to study. I think now we need to actually do something.”

Final thoughts

Reflecting on the techUK discussions, it seems that the UK is in a strong but fragile position, and time is of the essence. And the question facing the sector now seems to be whether the coordination required can happen quickly enough.

Given all this information, it is possible that photonics could be a fantastic driver in positioning the UK as a serious tech competitor, as long as companies and clusters are encouraged and supported to stay the course in the UK.

As Daniels pointed out, the UK hasn’t achieved this yet, and as much as we can talk a good talk, one has to wonder if we haven’t heard these conversations before. Different tech, different industries, but the same rallying talks followed by little investment or follow-through. Only time will tell if, this time, things will be different.