Author: Shazan Siddiqi, Senior Technology Analyst at IDTechEx

The company that changed ground transportation triggered a huge wave of investment by supporting the future of Advanced Air Mobility. More than 300 new electric vertical take-off and landing (eVTOL) aircraft manufacturing startups were established over the course of the following few years, each grabbing a piece of the $8.5 billion in funding that has been poured into the industry as of the end of 2023.

Now that the industry has received significant financing and crucial assistance from governments and regulators, it is imperative that they demonstrate their commitment to decarbonising aviation. In 2023, several new electric aircraft successfully demonstrated their technology. The upcoming challenges, however, are significant. Regulators must ensure safety and establish clear flying rules, while the public must be convinced of the aircraft’s sustainability and societal benefits.

IDTechEx’s report, ‘Air Taxis: Electric Vertical Take-Off and Landing (eVTOL) Aircraft 2024-2044: Technologies, Players’, predicts that unit sales of eVTOLs will exhibit a 25% CAGR for the period 2024–2044. IDTechEx’s research also indicates applications where eVTOL aircraft could provide a faster, more direct, and flexible journey at a lower cost than competing transport modes.

Here is what to expect from the eVTOL market in 2024 and beyond.

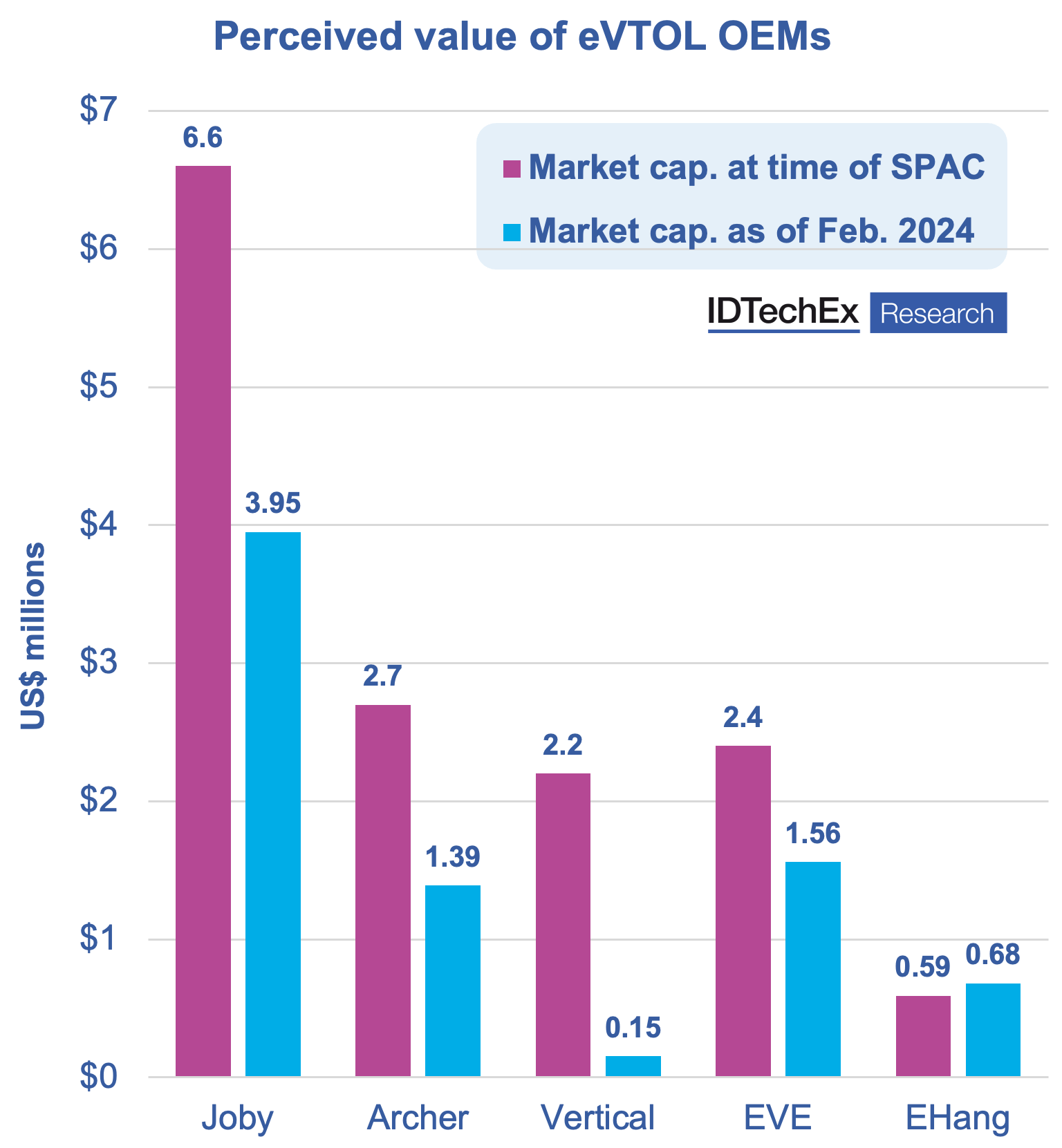

Changing market landscape

It is extremely doubtful that even 10% of the current 300 eVTOL manufacturers would make it through certification and into production, much alone becoming profitable. According to IDTechEx research, there will only be under 25 commercial eVTOL manufacturers (~5%) in ten years. In 2024, companies that didn’t raise enough capital during the abundant investment funding period may face a tough time. Slipping market entry timelines make it harder to secure funding. Finally, raising money for aircraft development will become more challenging, especially when top players will start operating commercially.

Chinese manufacturers eHang and Autoflight are emerging as early commercial operators of eVTOLs. Looking to the west, prominent companies with an eVTOL aircraft assessed at a high TRL and likely to come to market earlier compared to competitors include Archer (Midnight), Beta Technologies (ALIA), Lilium (Jet), Volocopter (Volocity), and Joby Aviation (S4). First mover advantage for any of these players is vital as more benefits will come next – income from early commercial flights will improve finances and attract additional funding. The IDTechEx report provides OEM updates and benchmarks eVTOLs based on performance metrics like range, payload capacity, and cruising speed.

Advancements in battery technology

Batteries are the heart of eVTOL aircraft. eVTOL batteries must provide high power for long periods to enable vertical takeoff, be light enough to sustain reasonable flight times and cargo loads, demonstrate good durability to provide a long life, and meet the highest commercial aviation safety standards. In short, AAM batteries must accomplish a great deal to enable electric flight.

Batteries used in automotive or other commercial applications have not been optimised to meet the correct balance of safety, power, energy, cycle life, charge time, and cost requirements for eVTOLs. While many existing and emerging battery technologies can be applied to eVTOLs, dedicated research and development are continuing to unlock the potential of battery electric flight. While automotive battery development has a strong focus on reducing cost, the eVTOL industry is actively working to reduce battery weight while increasing power and energy.

Aviation batteries will dramatically improve in the coming years, with IDTechEx forecasting an energy density improvement of 2–3% per year. Battery cell development has rapidly improved over the past decades, and today, cells are available with energy densities of greater than 300Wh/kg and power densities of greater than 3kW/kg.

Furthermore, IDTechEx research finds that silicon anode material can allow for considerable improvements in specific energy and energy density over state-of-the-art Li-ion cells. Silicon-dominant anodes will enable faster charging and higher power compared with graphite anode cells. Silicon also increases the discharge capacity of the battery cell; thus, the power provision at low SOC is significantly improved. The IDTechEx report provides details on OEM-supplier relationships and highlights battery technologies being used by industry frontrunners.

Ground infrastructure to play catch-up

With aircraft only a few years away from certification, 2025/26 for the first ones, the infrastructure progress has not kept up with the OEMs’ pace, falling behind. While at entry into service, the majority of eVTOL aircraft will operate out of existing infrastructure (airports, heliports); as the market develops and grows, these vehicles will use their unique performance capabilities to land on the top of buildings and other suitable spaces in crowded urban areas.

The general message from the regulators currently is that they would like to see safe operations from existing airports and heliports before new vertiports will be licenced. IDTechEx research finds opportunity for dual-use landing sites in the short term that can absorb traditional helicopter movements before electric operations can begin.