Graham Maggs, Director of Marketing, EMEA for Mouser Electronics has detected glimmers of light.

“There are some hints, the book to bill is better,” said Nigel Watts, Chief Executive Office of Ismosys.

Rob Rospedzihowski, President, Sales for Farnell in EMEA noted trading conditions were ‘still tough’, adding that Farnell was buffered by not being reliant on one industry sector or technology.

He added that conversations with capacitor suppliers suggest a tightening of lead times.

Georg Steinberger, Director at FBDi, the German component distribution association, sees rays of hope: “2019 was certainly worse than expected but, in spite of all skepticism and political paralysis, we expect to see a positive trend next year, and a return to former strong performance levels in 2021. The turnaround starts in people’s heads.”

Steve Rawlins, Anglia Chief Executive Officer was less optimistic, said: “If anything it’s got worse over the past three months,” he commented. He puts the market down by seven to ten percent. There’s still lots of inventory in the channel, and customers who stocked up earlier this year have excess inventory.

“On the other hand it’s not 2008. The world hasn’t stopped and companies are not going broke.”

It’s a point well made. 2019 can be dubbed ‘The Hangover Year’. Last year’s growth was phenomenal – as an example Mouser sales were up 46% – and as product shortages bit, companies ordered more and more product to ensure production lines kept running.

Emphasising this point Graham Maggs at Mouser observed, “We are looking at a flat year for sales in 2019. If you took the large electronic manufacturing services (EMS) companies out of the equation, we are showing sales growth this year in smaller EMS houses where a fair amount of design for production potentially takes place and growth in education, start-ups, hobbyists and makers.”

Maggs and Watts at Ismosys agreed the fundamentals of the industry are sound. 5G, IoT and electric vehicles will all drive demand for components. It’s the political uncertainties undermining confidence, so the curtain needs to come down on Brexit and the US-China trade row.

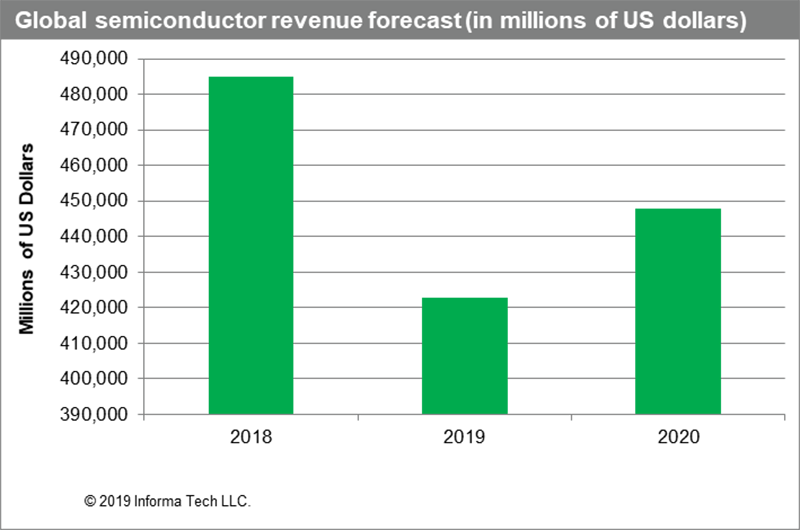

Research company IHS Markit Technology pulls no punches in its latest semiconductor market forecast.

The semiconductor industry is undergoing a brutal downturn in 2019, a drop so powerful, said the company, that it can only be ended by an even more formidable force: the massive economic impact exerted by the deployment of 5G technology.

It forecasts that following a 12.8% plunge in 2019, global semiconductor market revenue will rebound to 5.9% growth in 2020, an 18-percentage point swing. Global revenue will rise to $448 billion next year, up from $422.8 billion in 2019.

The deployment of 5G will be the main factor propelling this recovery, not only because of the renewed growth it will bring to the wireless industry, but also due to the wider benefits the wireless technology will bestow on global businesses and economies.

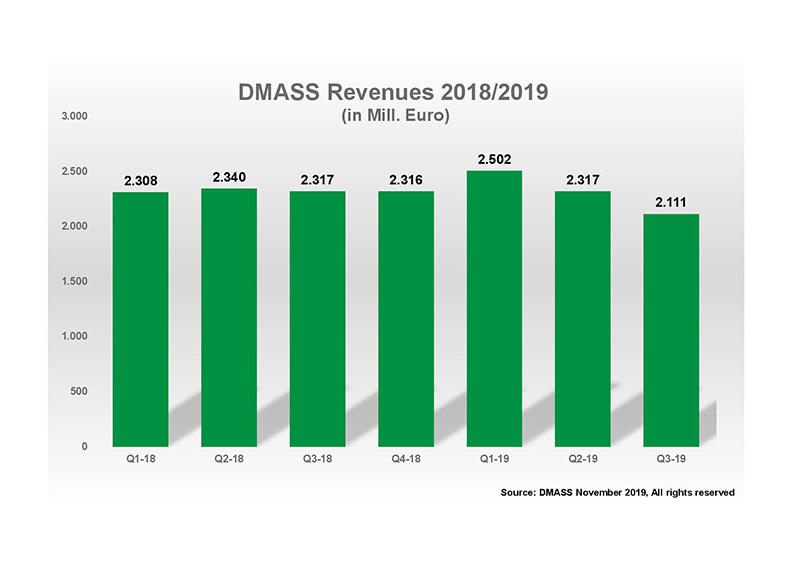

Semiconductor distribution in Europe declined sharply in the summer quarter. According to DMASS, sales in the European Semiconductor Distribution Market fell 8.9% to €2.11bn. The first nine months of 2019 still benefited from a stronger first half and “only” declined by 0.5% to €6.93bn.

In his role as chairman of DMASS, Georg Steinberger, remarked: “A slowdown in customer bookings throughout the year now materialised in a not surprising revenue decline. It is a mix of factors that is driving the slowdown – external and internal – and most of them will accompany us for a while.

“There is more caution and scepticism in the market than necessary, as we think that the opportunities for technology are still great. We expect the market to return during 2020.”

At country and region level, the situation is rather uneven. While in Q3 Germany, France and Italy declined double-digit, the UK actually grew by 1.6% and Eastern Europe held up with 0.5% growth.

Among the major markets, Germany fell by 12.9% to €618m, Italy dropped 13.1% to €168m, France shrank by 15% to €132m while UK sales rose 1.6% to €159m. The Nordic countries (including the Baltic States) by 3.7% to €183m. Eastern Europe edged forward 0.5% to €380m.

Steinberger added: “No big change to previous quarters. Countries with a huge share of contract manufacturing continue to grow or at least maintain their momentum, while OEM-driven markets experience a bigger slowdown or lose more business specifically to Eastern Europe, which has a strong contract manufacturing base. The most surprising aspect of this quarter is the resilience of the UK against the current Brexit frenzy.”

With 2019 almost done and most probably finishing slightly negative, the question is what 2020 will bring.

Steinberger said: “We believe that we will see more disruptive innovation in the next few years and more opportunities for distribution.”

And companies are investing to accrue the benefits of those opportunities. Digi-Key is plunging $400m on a new state-of-the-art distribution facility at its Thief River Falls headquarters. Slated to start operations in 2021, it will enable the distributor to process orders from receipt to despatch in 20 minutes.

Mouser Electronics is adding another 125,000 square feet of warehouse capacity which will come on stream next year.

Farnell is investing $60m in a new 362,000 square feet distribution centre in Leeds which will be ready for business early next year. “It will double the capacity of our shipments on a daily basis,” said Rob Rospedzihowski.

The extra capacity will be needed, as the distributor adds to the depth of its inventory. “We are talking to all our major vendors,” added Rospedzihowski. “More parts will be added and alongside that we have been undertaking a gap filling exercise to ensure we can cover all technology demands.”

Encouragingly there is also no sign of a let up in design activity.

“Design-in is going great,” said Nigel Watts at Ismosys, with strong activity at the company’s European design centres.

Anglia’s Steve Rawlins has a similar story with one caveat. “The designs are happening, we have taken on more field applications engineers to support them, but they are stalling at the manufacturing stage.”

Remarked Watts, “At some point companies will have to take their foot off the product pipeline.”

Rob Rospedzihowski highlights Farnell’s work with sister company Avnet Integrated to deliver designs based around the Raspberry Pi and BBC Micro computers, which have arrived via Farnell’s element14 design community or the Hackster hardware development community.

“It’s taken us into new markets including breweries, coffee makers and retail,” he added.

Predictions for 2020 are understandably cautious and diverse. Nigel Watts is looking for an upturn late in Q1 or Q2. Graham Maggs is hopeful for Q2. Both Rawlins and Rospedzihowski feel a more likely scenario is an upturn in the second half of the year.

“It’s not going to be a flick of the switch,” said Rospedzihowski. There are too many factors – Brexit, US-China, the German economy – to be settled.”

Whoever said in quiet times you can put your feet up was a liar.