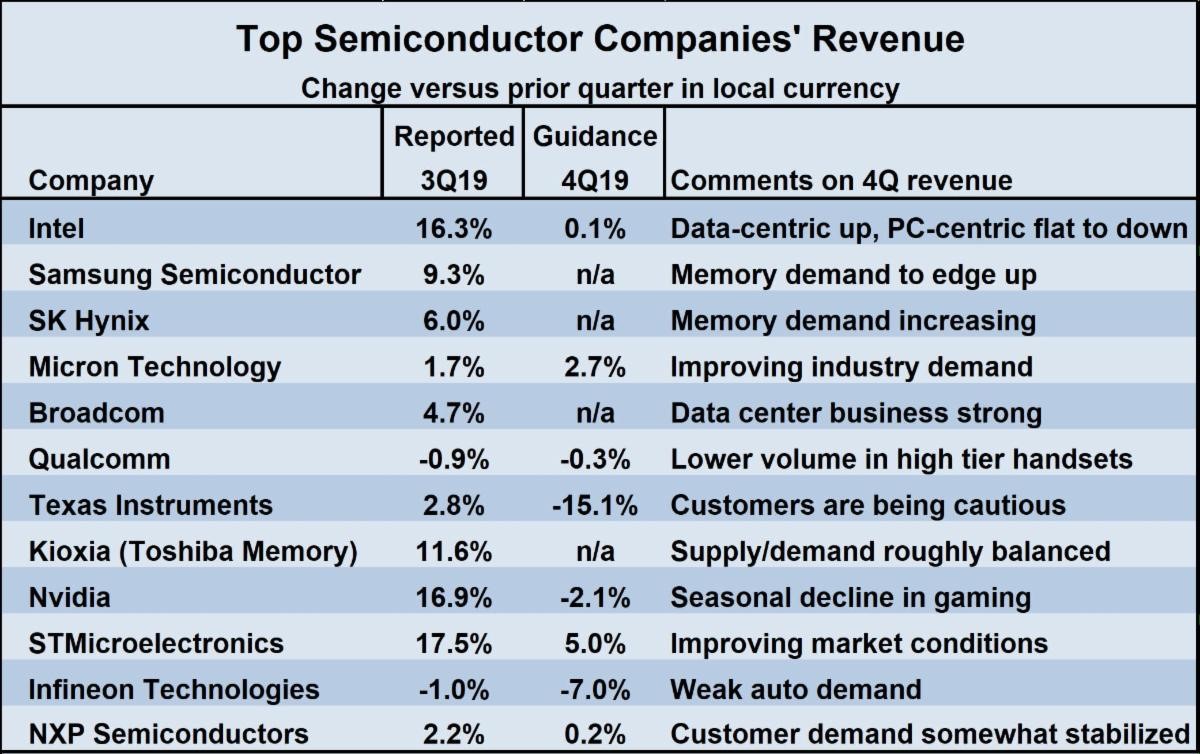

Reported revenue results from the top semiconductor companies demonstrate the pickup. 3Q 2019 revenues versus 2Q 2019 were up by double digits for four the of the twelve companies below, led by STMicroelectronics’ 17.5%.

Six companies had single digit increases while two (Qualcomm and Infineon) were down about one percent. The guidance for 4Q 2019 is mixed. Texas Instruments, Infineon and Qualcomm expect quarter-to-quart revenue declines. Intel, Micron Technology, STMicroelectronics and NXP Semiconductors expect single digit revenue gains.

The memory market appears to have stabilised. The major memory companies – Samsung, SK Hynix, Micron and Kioxia (previously Toshiba Memory) – all had quarter-to-quarter revenue gains in 3Q 2019 and all see demand improving in 4Q 2019.

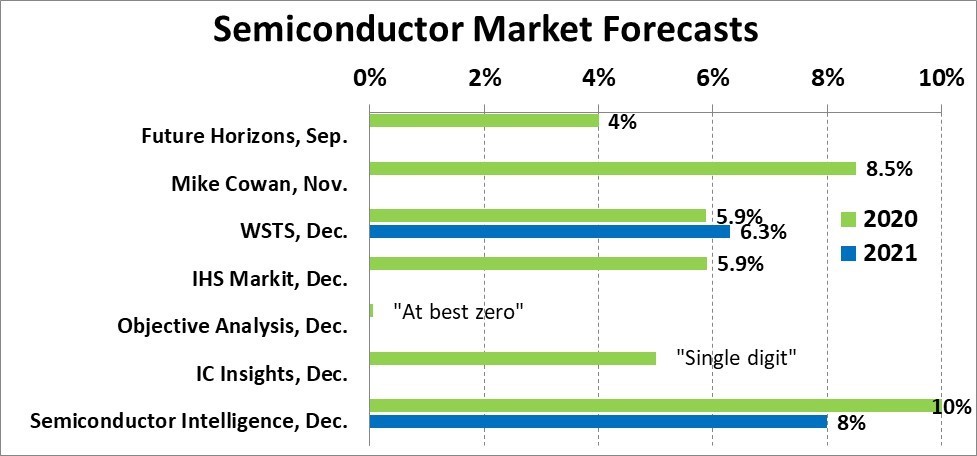

The semiconductor market recovery in the second half of 2019 will lead to growth in 2020. Objective Analysis is the most pessimistic, forecasting 2020 to be up ‘at best zero’. IC Insights projects single digit growth. Future Horizons, usually the most optimistic, expects four percent. WSTS and IHS Markit are both at 5.9%. The highest projections are Mike Cowan’s 8.5% and our Semiconductor Intelligence’s 10%.

Looking to 2021, WSTS expects 6.3% growth, similar to 2020. Semiconductor Intelligence expect 2021 to moderate slightly to eight percent from ten percent in 2020.

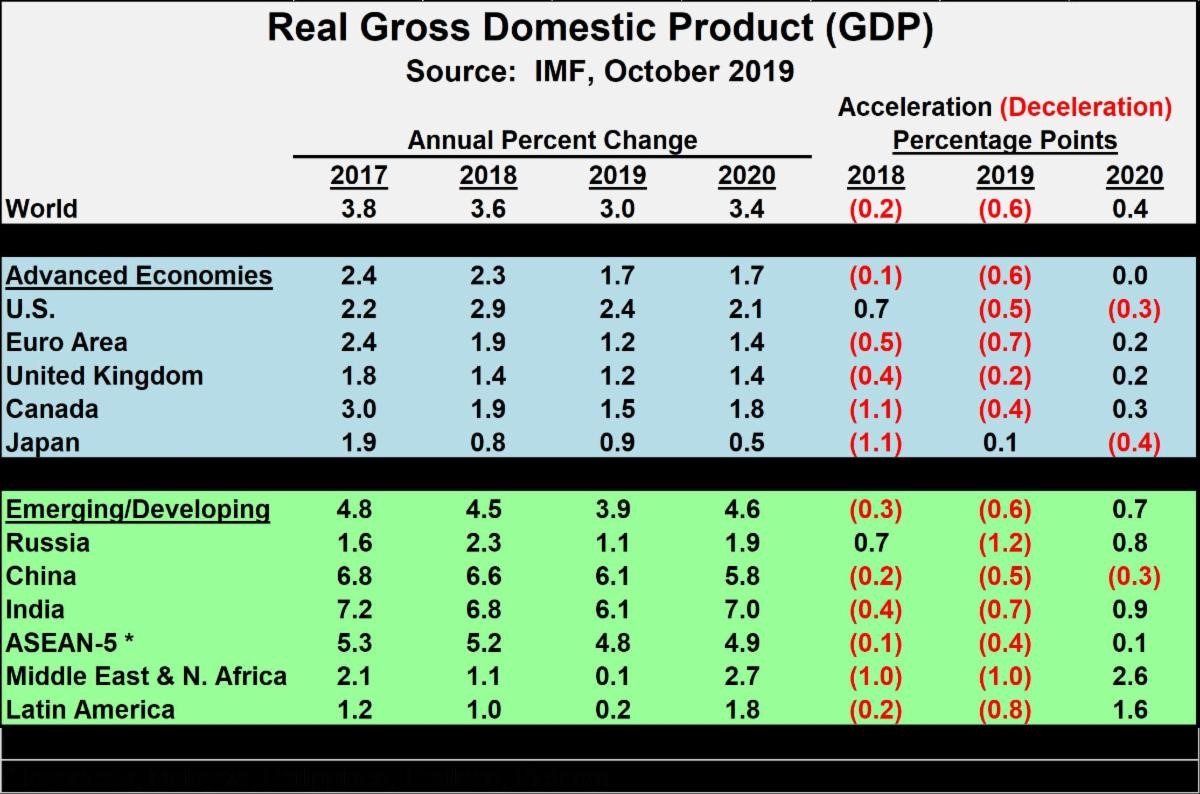

The 2020 semiconductor market recovery will be driven by an improving economic outlook. The October forecast from the International Monetary Fund (IMF) calls for World GDP to improve from 3.0% growth in 2019 to 3.4% growth in 2020. The advanced economies should have the same growth of 1.7% in 2020 as in 2019.

A moderate growth acceleration from the Euro area, United Kingdom and Canada will be offset by slowing growth in the US and Japan. Emerging and developing economies will drive stronger global growth in 2020. Although China growth will continue to slow, growth will accelerate in Russia, India and the ASEAN-5 (Indonesia, Malaysia, the Philippines, Thailand and Vietnam). The Middle East and Latin America are expected to rebound from near flat growth in 2019 to growth in the two percent to three percent range in 2020.

Recent developments point to stronger economic growth in 2020. Last week the US and China reached a preliminary agreement on trade which will delay additional US tariffs on Chinese goods which were set for 15th December in return for China purchasing more US agricultural products. Last week in the UK, the Conservative party won the election which puts Brexit (UK exiting the European Union) back on track.

The 2020 semiconductor market will also benefit from a return to growth of smartphones. IDC projects 1.5% growth in smartphone unit shipments to 1.4 billion in 2020 after three years of decline. The smartphone growth will be driven by 190 million 5G smartphones expected to ship in 2020. IHS Markit predicts key 2020 market drivers will also include servers and automotive.

Although the is still much uncertainty in the global economy, the semiconductor market has turned the corner towards recovery. We should see a much stronger market in 2020, with growth momentum continuing into 2021.