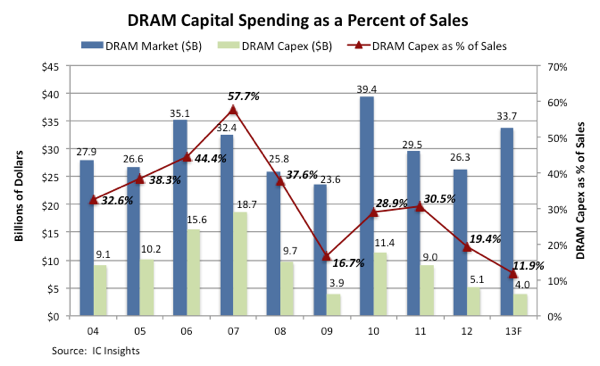

The DRAM market is forecast to reach $33.7 billion. This means DRAM capital spending as a percent of sales is forecast to fall to an all-time low of only 11.9% this year (Figure 1). Lower-trending capex investment for new DRAM fabs and process technology upgrades have contributed to rising average selling prices for DRAM so far in 2013. For the year, the DRAM average selling price is forecast to jump 40% and lift total DRAM market growth 28%.

Figure 1

The ability of suppliers to spend large sums of money to build a brand new wafer fab or to upgrade existing fabs has become nearly prohibitive for all but the leading DRAM manufacturers. With the price of a new wafer fab approaching $5 billion, only Samsung, SK Hynix, and the new Micron-Elpida will be able to continue investing in new and/or upgraded facilities this year.

Samsung perennially has had the DRAM industry’s largest capital expenditure budget, which has allowed it to reduce costs and offer advanced products more quickly than its competition. From 2010-2013, Samsung’s cumulative four-year DRAM capital spending ($10.95 billion) is forecast to far exceed the amount spent by either of its two nearest rivals—SK Hynix, $6.1 billion; and Micron, $5.1 billion—over the same period. (DRAM capex by the newly formed Micron-Elpida venture amounts to approximately $7.8 billion over the four-year span).

Perhaps more telling is how quickly the level of DRAM capex spending falls off after SK Hynix and Micron. After investing heavily to bring 50nm- and 40nm-class processes to their 300mm wafer lines, Taiwan-based suppliers are out of cash. Facing intense pressure from the world’s leading DRAM vendors, second-tier players like Nanya, Powerchip, and Winbond are having to look for niche markets in order to revive their respective IC businesses.

In the five-year span from 2004-2008, DRAM capital expenditures as a percent of sales averaged 42.1%. In contrast, that ratio over the five-year span from 2009-2013 is forecast to average 21.5%. Since only the top DRAM suppliers will be able to continue investing in new facilities, IC Insights forecasts the ratio of DRAM capex to sales to be in the 15-20% range through 2017, greatly reducing the potential for huge swings in the market based on too much or too little capacity in the system.