According to Adam Fletcher, IDEA Chairman, Q3 ’20 performance figures were essentially ‘flat’ on the previous quarter but in-line with his members’ forecast, which given the turmoil in overall European economic activity he feels is probably a reasonable result as it is significantly better than many other markets sectors.

“At the end of Q2 ‘20 IDEA members were optimistically looking forward to seeing a return to low growth into the second half of 2020 but as we move towards the end of the year with COVID-19 related lockdowns and associated disruption across Europe, this is now looking unlikely,” said Fletcher. “Q4 is historically a weak quarter in European electronic components markets and we are now forecasting a modest decline for the entire year in the range (10%)-to-(12%) when compared to 2019.”

Each month IDEA collates the statistical data reported by its member associations throughout Europe, which it then consolidates before publishing the figures as headline information. IDEA uses three primary metrics in its reporting process: ‘Billings’ (sales revenue invoiced, less credits), ‘Bookings’ (net new orders entered), and the ratio of the two known as the ‘Book to Bill’ (or B2B) ratio.

A positive B2B number – i.e. greater than one – indicates growth in electronic components markets but a number below 1 is evidence of a decline: “All three metrics are important, but the consolidated ‘Billings’ number is possibly the most useful indicator for many organisations in the electronic components supply network,” explained Fletcher. “The Billings metric is the most accurate indicator of average sales revenue performance in Europe and organisations are able to use this figure to compare the European average with their actual operating performance”.

The data presented in the following graphics is shown in K€ Euros and where necessary, has been converted from local currencies at a fixed exchange rate for the year.

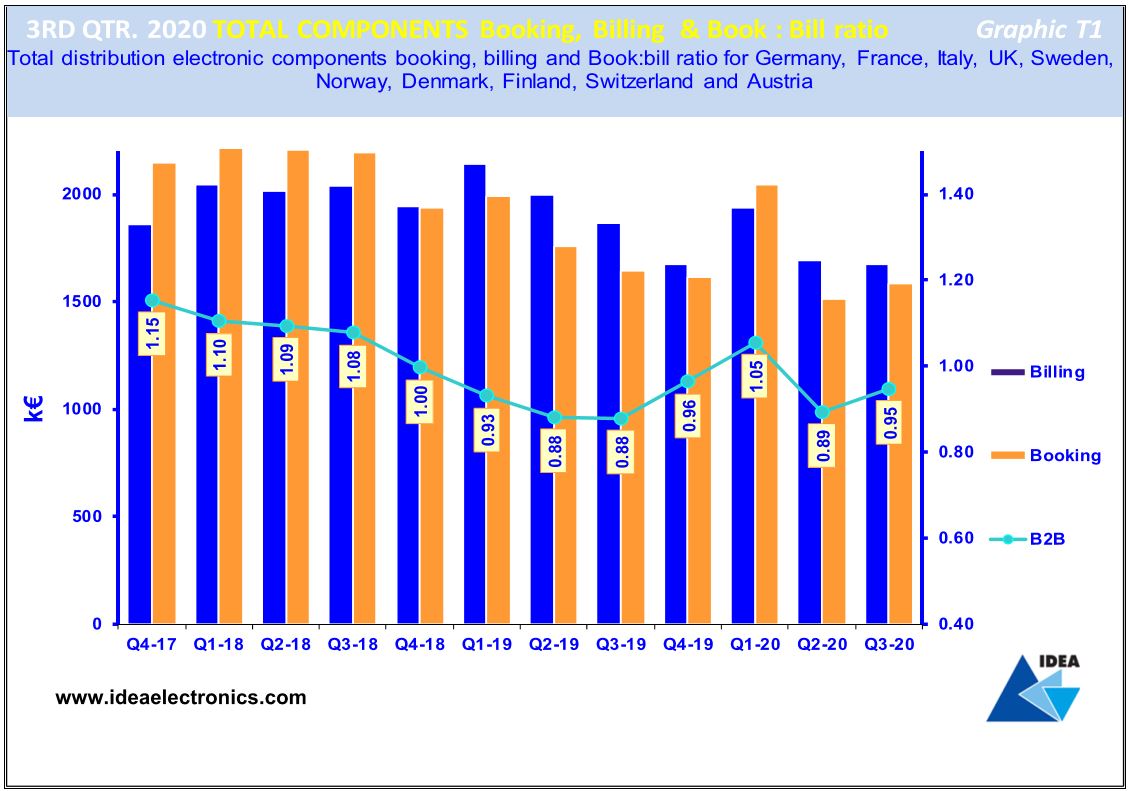

Overall Q3 ‘20 Bookings, Billings & B2B trends – European “Book to Bill” remains negative in Q3 ’20

Graphic T1 is a visual representation of twelve quarters of consolidated European ‘Billings’ and ‘Bookings’, together with the corresponding ‘Book-to-Bill’ (B2B) ratios.

A quick glance at the chart suggests that there was a slight improvement in Bookings in in the third quarter 2020 with Billings declining slightly compared to the previous quarter but suffered a more significant decline compared to the same period last year.

The B2B ratio improved from 0.89:1 to 0.95:1 but remained below unity. In effect the market slowed, confirming that customers were generally allowing their order cover to decline in Q3 ‘20 in response to widespread market uncertainties and limited visibility from their customers, despite electronic components manufacturer lead-times extending in this period.

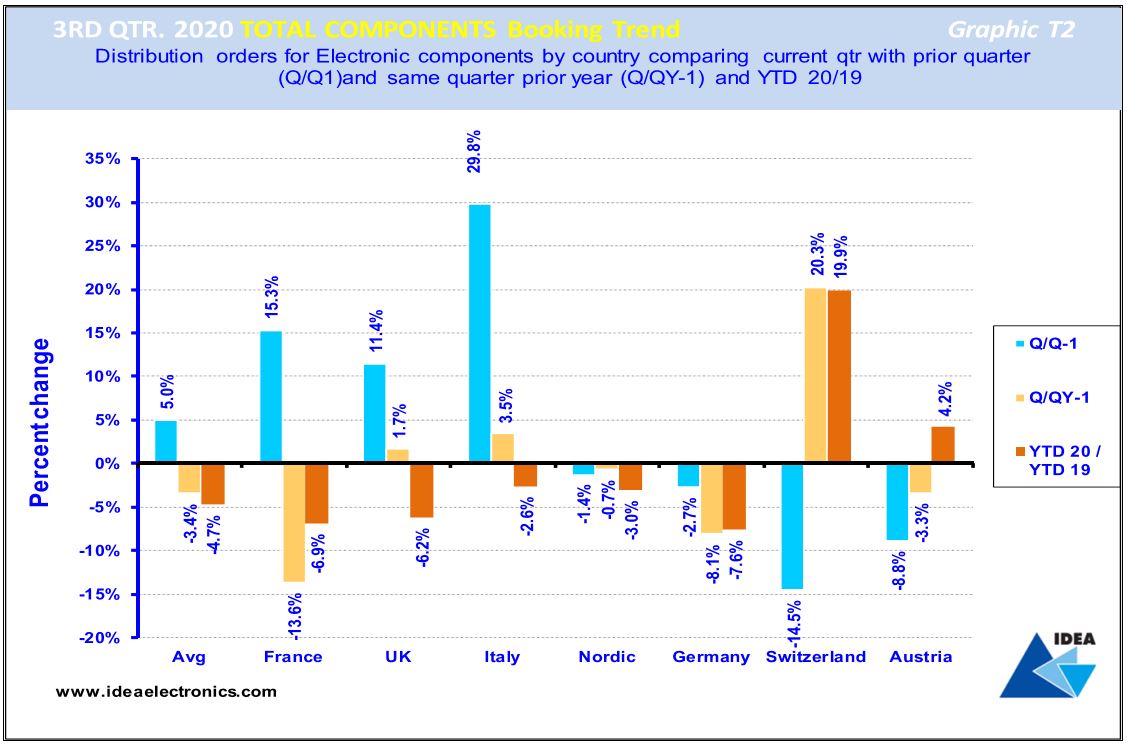

Q3 ‘20 Bookings Trend – European Bookings continue to decline into Q3 ’20

Graphic T2 compares the total electronic components ‘Bookings’ result achieved in each European country in Q3 ’20 and contrasts and compares these figures with the result they achieved in the previous quarter and those achieved in the same period last year.

The blue bar reveals that on average European ‘Bookings’ increased by five percent in Q3 ‘20 when compared to the previous quarter.

The light brown bar compares ‘Bookings’ growth by country in Q3 ‘20 with those in the same quarter 2019 and indicates that on average ‘Bookings’ declined by (3.4%) in this period.

The dark brown bar compares average ‘Bookings’ achieved in Europe year-to-date with the same period in 2019, revealing that the average Bookings growth rate declined by (4.7%) across Europe over the 12-month period, strongly suggesting that customers in the European market were reluctant to put order cover in place.

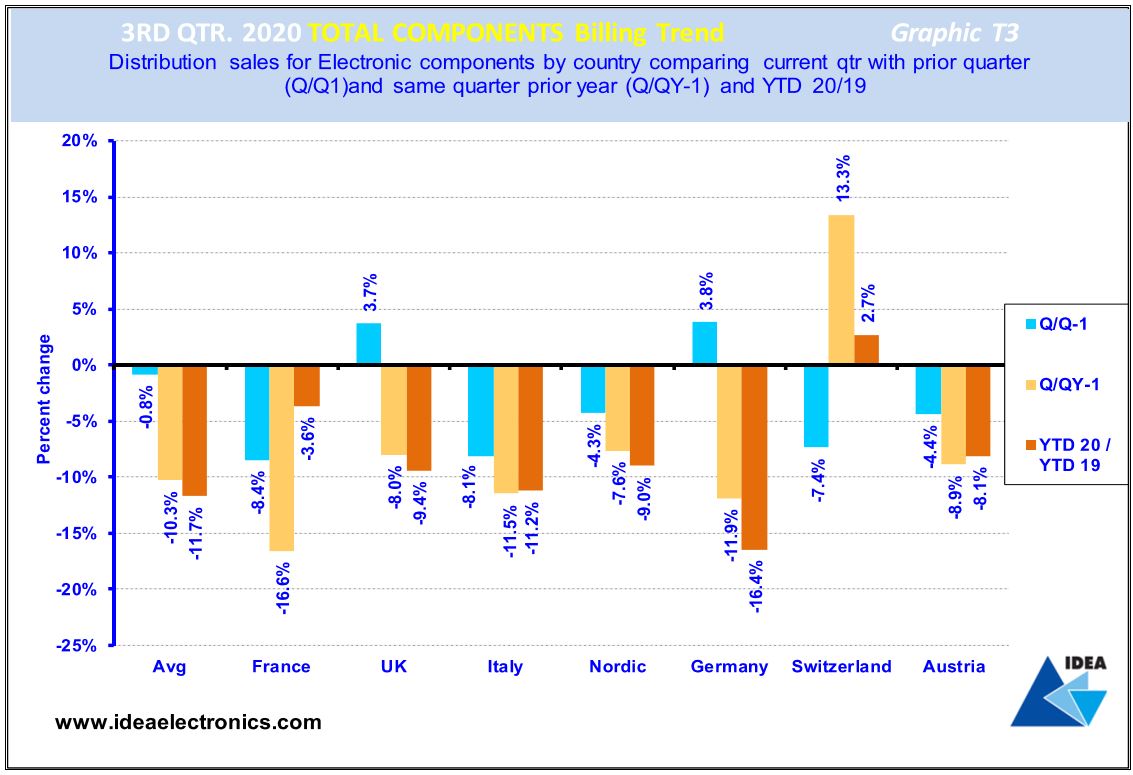

Q3 ’20 Billings Trend – European Billings decline in Q3 ’20, due primarily to COVID-19

Graphic T3 illustrates total electronic components ‘Billings’ achieved in European markets in Q3 ‘20 and contrasts and compares the results with the previous quarter’s results and those achieved in the same period last year.

The blue bars reveal that European electronic components markets experienced an average decline of (0.8%) in Q3 ‘20 when compared to the previous quarter.

The light brown bars compare Q3 ‘20 with the same quarter last year and shows that European electronic components markets suffered in the quarter year-on-year, with an average decline of (10.3%).

The dark brown bars compare current YTD ‘Billings’ with the same period 2019, revealing an average decline of (11.7%) across all European electronic components markets.

“Even given the COVID-19 pandemic this is a disappointing result but reflect what’s actually happening in the market,” Fletcher concluded. “IDEA members have become adept at trading in adverse conditions and remain hopeful that the low point in the current economic cycle has been reached and believe that growth will return to the electronic components supply network in 2021, despite the ongoing issues posed by COVID-19 in Europe”.