This growth is driven by surging demands in the AI, 5G, and automotive sectors. New entrants are entering the market to meet the rising AI customer needs, resulting in substantial demand for substrates. All market participants are making substantial investments to meet these requirements and accommodate the escalating demand, as stated by Yole Intelligence in its semiconductor packaging report, ‘Status of the Advanced IC Substrate Industry 2023.’

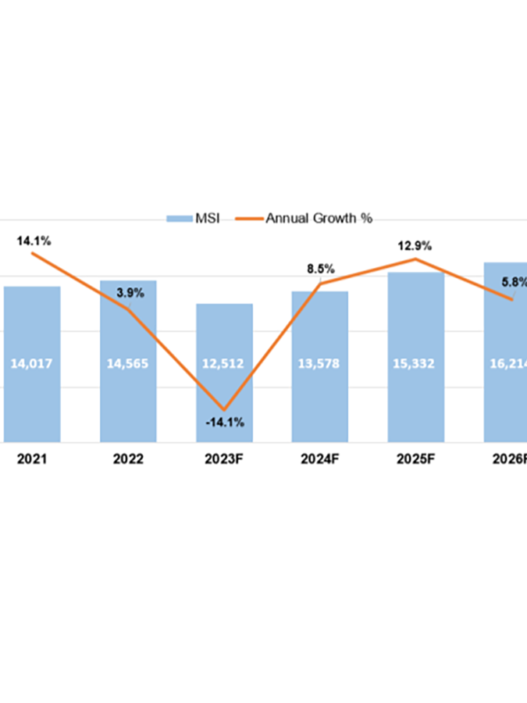

In this advanced IC substrate market, Yole Intelligence, a part of Yole Group, anticipates the SLP market to grow from $2.9 billion in 2022 to $3.6 billion by 2028, primarily driven by high-end smartphones. The emerging laminate substrate technology, ED, is expected to surpass 1.2 billion units in production by 2028, with revenue reaching $900 million.

Yole Intelligence has developed a comprehensive advanced packaging technology and market report for the IC industry, providing insights and forecasts. In its “Status of the Advanced IC Substrate Industry 2023” report, the company offers an overview of the industry, ecosystem, and technology for each substrate platform.

Bilal Hachemi, PhD., Technology and Market Analyst, Packaging within the Semiconductor, Memory, and Computing Division at Yole Intelligence, part of Yole Group, highlights the potential of a novel substrate core material, Glass Core. This innovative solution in the advanced IC substrate market is making strides, particularly in AI and server applications.

The epicentre of advanced IC substrate manufacturing is in East Asia, specifically Taiwan, South Korea, and Japan, with Taiwan playing a pivotal role. China is also making significant advancements with unprecedented investments, positioning itself for future market dominance.

Japanese players like Meiko and Ibiden hold substantial market shares and serve as key SLP suppliers to Samsung. Chinese players, such as AKM Meadville and KinWong, are entering the market to cater to domestic demand from Huawei, Xiaomi, and Oppo. SLP adoption primarily pertains to high-end applications due to its higher cost, hindering widespread adoption. However, the SLP market is expected to gradually grow, driven by increasing demand for 5G smartphones and potential adoption in the medical and automotive sectors.

Vishal Saroha, Technology and Market Analyst Packaging at Yole Intelligence, notes that Taiwanese companies, including ZD Tech, Compeq, and Unimicron, dominate the SLP market, accounting for almost 60% of total SLP revenue in 2022. AT&S, based in Austria, is the sole contender in Europe, aiming to break into the top three soon. Currently, no substrate supplier in the US ranks among the top twenty. Thus, the production of advanced substrates remains highly concentrated in Asia.

To diversify supply chains and enhance local resilience in Europe and the US, more companies are considering investments in the advanced substrate industry, with local government incentives potentially driving this trend. New entrants are entering the advanced substrate sector to meet the needs of AI market leaders.