The basis for this is the demographic development of the population and an increasing number of chronically ill people in need of long-term care.

Other driving forces are high investments by emerging countries in the health sector and new or further technological developments such as digitalization, the use of artificial intelligence, developments in sensor technology and also individualised medical technology.

Not only new devices and protective mechanisms for COVID-19, but also the general introduction of modern technologies is causing changes in the business models of medical technology manufacturers. Here, component distributors can provide support with integrated logistics solutions and a permanently expanded product portfolio.

They advise the buyers and developers of the Medtech companies independently of manufacturers in the selection and design-in of specific components and modules.

In this way, the developers of technical products benefit in particular from new designs. After all, it is important to plan for components with delivery times that are as manageable as possible. In addition, the components of different manufacturers must function efficiently with each other if innovative systems are to achieve their full performance.

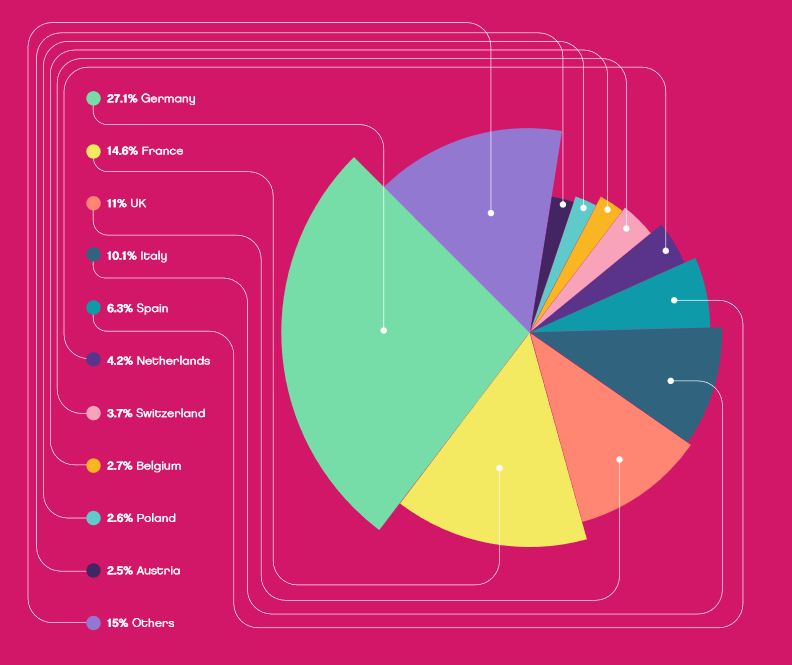

Figure 1: European medical device market by country 2018. Source: MEDTech Europe

Versatile flexibility

In most manufacturing companies, the on-time delivery of raw materials and components is part of everyday life. Nevertheless, digital procurement processes can help to ensure that the supply chain is as seamless as possible. Component distribution serves the different requirements of the manufacturers and is a reliable partner for the companies. For example, through the electronic exchange of structured business-relevant data. With the help of EDI (Electronic Data Interchange) interfaces, data entry errors can be avoided and order processing can be optimised by automatically triggered processes.

Developers and purchasers not only offer distributors comprehensive services, they also provide detailed information on the latest products. In addition, distribution ensures the availability of components, especially in difficult times, with a comprehensive warehouse and foresighted stock-keeping.

Driving force medical technology

Furthermore, Component Distribution sees itself as a trend scout. Therefore, the companies are geared to be able to meet the short to medium-term requirements of the industry through optimal component availability. In the field of medical technology, experts are expecting future-oriented developments in the coming years, which should ensure more efficient healthcare. These include digitally networked medical technology units and newly developed, independently operating automation and robotics solutions. These smart devices should, for example, enable efficient sample throughput in the laboratory area with lower resource consumption.

Synergy effects will also be increasingly evident in the e-health sector, for example, new technologies will make it possible to detect diseases earlier and make more reliable diagnoses. This could shorten or even completely avoid hospital stays.

On the other hand, other achievements such as telemonitoring, digital assistance systems and robotics can offer many patients a higher degree of mobility. The corona crisis in particular has brought 3D printing to the forefront to produce safety equipment and other devices. All applications could not function without components.

Among them, sensors are playing an increasingly important role in many applications, making medical devices safer and more powerful while simplifying operation. Wearables also benefit from intelligent sensors. Regardless of the final application, distribution with starter kits and reference designs can help to shorten evaluation and development phases. This in turn allows the manufacturer a faster entry into mass production.

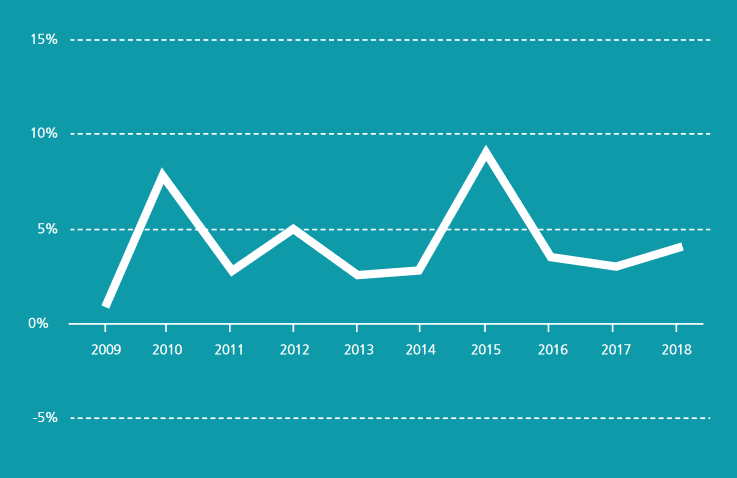

Figure 2: European medical device market growth rates 2009-2018 : The European medical device market has been growing on average by 4.2% per annum over the past 10 years. Demand fell in 2009 due to the economic crisis, resulting in a growth rate of only 1%. The market recovered in 2010, since then the annual growth rate has varied between 2.6 and 9.3% in the European medical device market. Source MedTech Europe

Medical technology as job engine

The development and production of internationally competitive medical technology is also a job engine. More than 730,000 people were employed directly in the European medical technology industry, of which 97,600 in the UK, which underlines the importance of this industry in the European economy. Most of the nearly 27,000 medical technology companies in Europe are based in Germany, followed by Italy, the UK and France. The majority (around 95%) are small and medium-sized companies with less than 50 employees. The European medical technology market is estimated at roughly €120 billion in 2018.

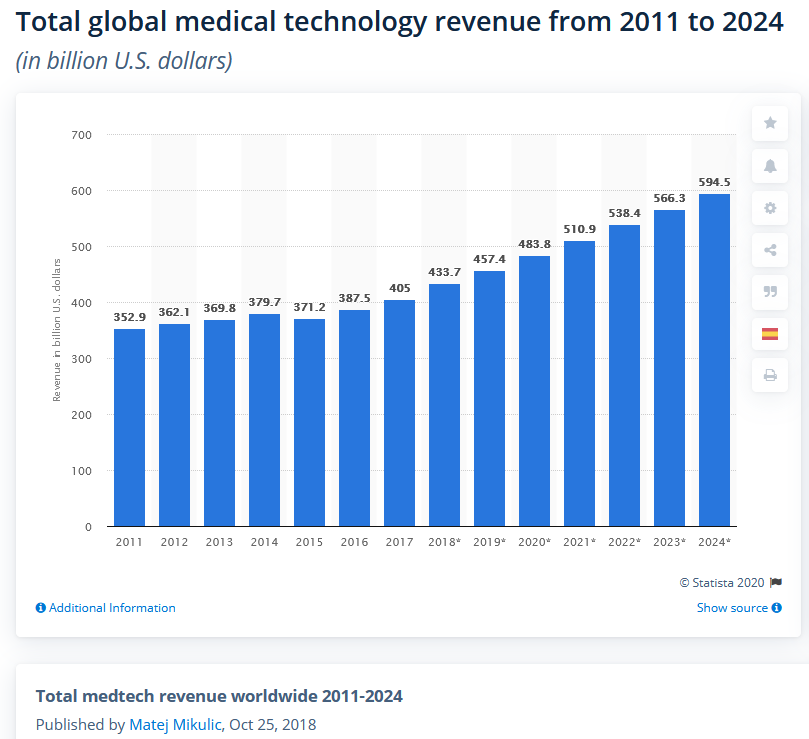

According to surveys by the Statista Research Department, leading global medical technology companies generated total sales of around 434 billion US dollars in 2018. Nearly 40 percent of global production is located in the USA, where six of the ten leading medical technology companies are based according to the study. GTAI – Germany Trade & Invest (the business development agency of the Federal Republic of Germany) rates the British market for medical technology as the sixth largest medical technology market in the world and the third largest in Europe (after Germany and France).

Even if the planned withdrawal of the British from the EU makes market forecasts difficult, GTAI refers to figures of the consulting company Fitch Solutions, which expects an average annual industry growth of 4.6 percent nominal on a pound sterling basis for the period 2019 to 2023. Structural growth factors are the growing and ageing population and the increase in chronic conditions and lifestyle diseases (obesity, diabetes, cancer, etc.).

Legal challenges

At the same time, medical technology companies are confronted with new legal requirements such as the new regulation for medical devices 2017/745/EU, which was delayed for one year until 26 May 2021 due to the COVID-19 pandemic. EU-MDR is expected to change the medical device law in a lasting way, introducing major changes to how medical device manufacturers obtain CE marking and maintain access to the European market. The new regulation establishes uniform criteria for so-called Notified Bodies for the approval of medical devices (approx. more than 500,000) and regulates the approval of clinical trials of medical devices.

The associated framework conditions, such as legally compliant documentation, affect medical device manufacturers as well as providers of Electronic Manufacturing Services (EMS) and Original Equipment Manufacturers (OEM). The aim of the new framework conditions coupled with the regulations is to improve the quality, safety and performance of medical devices throughout Europe in order to protect patients and users.

In spite of Brexit the UK is affected due to its close economic ties to the EU. A national version, the UK MDR, was drafted for a transition period of ten months. With the revised MDR implementation date falling outside of the transition period, the UK market is waiting for guidance of the Medicines and Healthcare products Regulatory Agency (MHRA).

The medtech industry is confronted with complex legislation that requires immense knowledge of a wide range of issues. Accordingly, companies must adapt their business concepts to these regulations.

“In Germany, the FBDi Association offers an important platform for regular exchange among distributors. Its Competence Circles range from brand assessments to environmental regulations and provide valuable specialized knowledge”, Falke explained. “After all, an electronic product may only be marketed and put into operation in the EU if it complies with the provisions of all EU directives applicable to the product.”

The constructive exchange of member companies helps to comply with specifications and eco-design guidelines – keyword FBDi Environmental & Conformity Compass, which will also be available as a web tool in the new edition.

The new EU directives in particular are driving the demand for innovative and sustainable concepts – and thus creating potential for distribution, which, with concentrated industry knowledge, can also broaden the manufacturers’ perspective. In addition, they support market participants with holistic solutions to fully exploit market potential. Enough opportunities, therefore, to play a driving role in this future market.