The rapid buildout of AI data centres is consuming a growing share of the world’s memory supply, leading to tech companies and electronics manufacturers increasing prices for their consumer goods.

Rising demand for High Bandwidth Memory (HBM) is pulling manufacturing capacity away from conventional Dynamic Random-Access Memory (DRAM) and NAND technology. According to IDC, DRAM prices have roughly doubled since early 2025 and, unlike past cycles, this represents a sustained reallocation of supply, not a temporary disruption.

McKinsey projects $7 trillion in data centre spending through 2030, with $5.2 trillion AI-focused, meaning the pressure on memory supply will only intensify in the near term.

A recent survey from the Global Electronics Association states that 62% of manufacturers report constrained availability or extended lead times and 82% report rising prices, including 33% citing significant increases. And just 14% expect conditions to improve in the next six months.

“AI isn’t just increasing demand, it’s reshaping who gets access to critical inputs. This is a fundamental reprioritisation of memory in the global electronics ecosystem,” said Shawn DuBravac, Chief Economist, Global Electronics Association. “As a result, manufacturers outside the AI supply chain are competing in a more constrained and less predictable market. This isn’t a short-term imbalance; it signals a longer-term shift where flexibility in design and supply strategy becomes a competitive differentiator.”

The impact on consumer electronics

2026 is certainly shaping up to be a year in which technology becomes more expensive.

Take smartphones as an example: for a mid-range device, memory can represent 15-20% of the total bill of materials with a high-end device being around 10-15%.

According to IDC, manufacturers whose business is mainly in the low end of the market are likely to suffer significantly. TCL, Transsion, Realme, Xiaomi, Lenovo, Oppo, Vivo, Honor, or Huawei will be affected substantially and will have no other choice than to pass the increased cost onto the consumer. Manufacturers such as Apple and Samsung are in slightly better positions with their long-term supply agreements meaning they can secure memory supply for 12-24 months. It does mean, however, that new models will likely have no RAM upgrades.

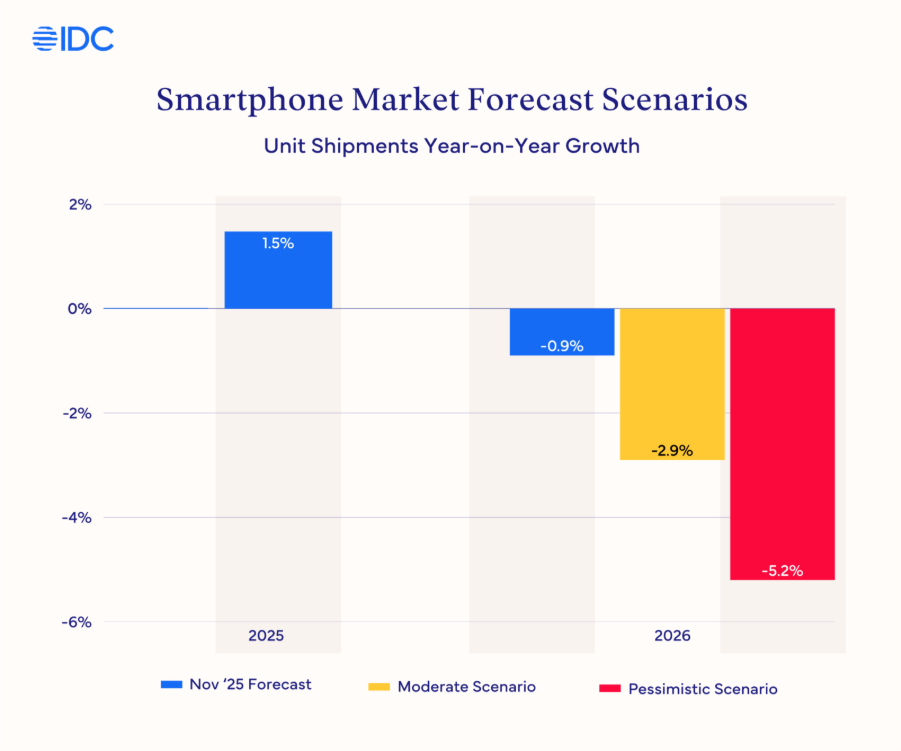

In the moderate downside scenario, the global smartphone market could contract by 2.9%. In the pessimistic downside scenario, the contraction could reach 5.2%.

Principal Analyst at Counterpoint Research Yang Wang said: “The impact is expected to continue through H2 2027, as it will take several quarters for memory supply expansion to materialize. Lower-end smartphones are likely to be affected the most, especially as LPDDR4 supply is shrinking faster than expected. OEMs are already responding with launch delays, streamlined portfolios, and specification trade-offs. We have also observed 10% to 20% price increases across some Android OEM portfolios in January 2026.”

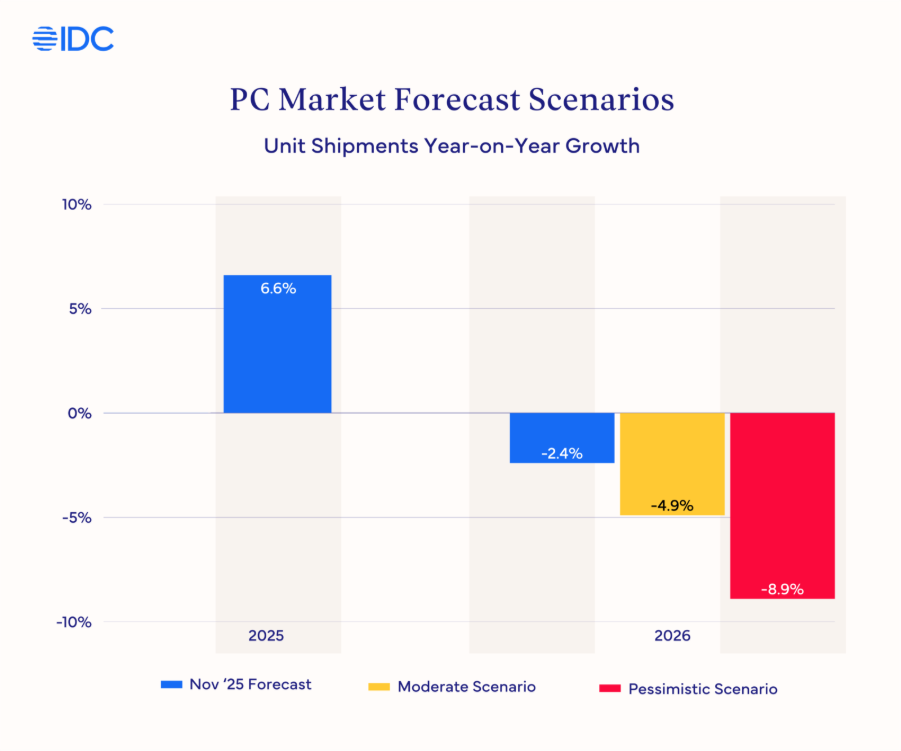

The PC market is no better. In the moderate downside scenario, the PC market could contract by 4.9%, compared with a 2.4% year-on-year decline in IDC’s November forecast. Under a more pessimistic scenario, the decline could deepen to 8.9%.

Lenovo, Dell, HP, Acer, and ASUS have already confirmed 15-20% price hikes.

More recently, Valve raised the prices of its Steam Deck OLED handheld gaming consoles by nearly £200, citing rising memory and storage costs. The 512GB OLED model now costs £649, up from £480. The 1TB model climbed even higher, from £570 to £780.

The company stated: “Steam Deck itself hasn’t changed; these new prices reflect the current state of component costs and other global logistical challenges across the industry as a whole.”

In February 2026, Steam had already acknowledged that widespread shortages of the Steam Deck were “due to memory and storage shortages.” That same month, Valve also postponed the announcement of pricing and availability for its new Steam Hardware lineup – including a new Steam Machine, Steam Controller, and Steam Frame VR headset – due to the same issue.

The tension was also felt across other gaming platforms with Microsoft increasing the price of the standard Xbox Series X to $649, while Sony’s PlayStation 5 recently jumped to $649.99 for the base model and $899 for the PS5 Pro. Nintendo will also raise the price of the Nintendo Switch 2 by $50 in September.

Advice for consumers

Anyone that’s considering buying a new laptop, smartphone, or gaming console should buy now and avoiding waiting.

This is potentially a permanent, strategic reallocation of the world’s memory supply. The three biggest memory manufacturers – Samsung Electronics, SK Hynix, and Micron Technology – have pivoted their already limited cleanroom space and capital expenditure toward higher-margin enterprise-grade components for AI infrastructure and data centres. And the consumer industry will pay the price.

It’s also worth considering the pre-owned, refurbished market which has, not surprisingly, seen a significant boost. Valve itself is actively promoting refurbished Steam Decks units as a more affordable alternative.

Also try to extend your current devices for as long as possible – delay upgrades where possible, invest in repair and maintenance to stretch the lifespan, and avoid unnecessary refreshes whilst the prices are high.

Most importantly, be wary of ‘shrinkflation’. A lot of consumer reports flag that some manufacturers may hold prices steady but quietly reduce the specs – less RAM, slower storage etc. It’s worth ready the fine print and checking the spec sheet to make sure you’re getting like-for-like value.