Early 2015's top 20 semiconductor suppliers analysed

IC Insights will release an update to the 2015 McClean Report in late May 2015. This update includes a discussion of the history and evolution of IC industry cycles, an update of the capital spending forecast by company, and a look at the top 25 1Q15 semiconductor suppliers (the top 20 1Q15 semiconductor suppliers are covered in this bulletin).

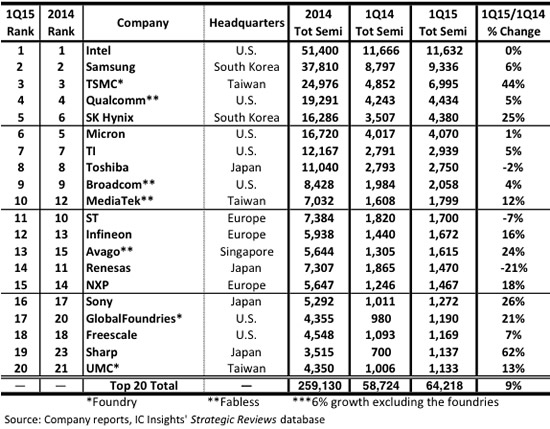

The top 20 worldwide semiconductor (IC and O S D - Optoelectronic, Sensor, and Discrete) sales ranking for 1Q15 is shown in Figure 1, below. It includes seven suppliers headquartered in the U.S., four in Japan, three in Taiwan, three in Europe, two in South Korea, and one in Singapore, a relatively broad representation of geographic regions. The top 20 ranking includes three pure-play foundries (TSMC, GlobalFoundries, and UMC) and four fabless companies.

It is interesting to note that the top four semiconductor suppliers all have different business models. Intel is essentially a pure-play IDM, Samsung a vertically integrated IC supplier, TSMC a pure-play foundry, and Qualcomm a fabless company. IC Insights includes foundries in the top 20 semiconductor supplier ranking since it has always viewed the ranking as a top supplier list, not a marketshare ranking, and realises that in some cases the semiconductor sales are double counted.

With many IC Insights clients being vendors to the semiconductor industry (supplying equipment, chemicals, gases, etc.), excluding large IC manufacturers like foundries would leave significant holes in the list of top semiconductor suppliers. As shown in the listing, the foundries and fabless companies are identified. In the April Update to The McClean Report, marketshare rankings of IC suppliers by product type were presented and foundries were excluded from these listings.

It should be noted that not all foundry sales should be excluded when attempting to create marketshare data. For example, although Samsung had a large amount of foundry sales in 1Q15, some of its foundry sales were to Apple. Since Apple does not resell these devices, counting these foundry sales as Samsung IC sales does not introduce double counting.

Figure 1: Q1 2015 top 20 semiconductor sales leaders, including foundries ($m)

Overall, the top-20 list shown in Figure 1 is provided as a guideline to identify which companies are the leading semiconductor suppliers, whether they are IDMs, fabless companies, or foundries. In total, the top 20 semiconductor companies’ sales increased by 9% in 1Q15/1Q14 (6% excluding the foundries), three points greater than the total worldwide semiconductor industry growth rate.

Although, in total, the top 20 1Q15 semiconductor companies registered a 9% increase, there were six companies that displayed under 20% 1Q15/1Q14 growth. Nine companies had sales of at least $2.0bn in 1Q15. As shown, it took just over $1.1bn in quarterly sales just to make it into the 1Q15 top 20 semiconductor supplier ranking.

There were two new entrants into the top 20 ranking in 1Q15 - Japan-based Sharp and Taiwan-based pure-play foundry UMC, which replaced U.S.-based AMD and Nvidia. AMD had a particularly rough 1Q15 and saw its sales drop 26% year-on-year. It currently appears that AMD’s 2013 restructuring and new strategy programs to focus on non-PC end-use segments have yet to pay off for the company (in addition to its sales decline, AMD lost $180m in 1Q15 after losing $403m in 2014).

Although Intel’s sales were flat in 1Q15, and it believes its 2015 sales will be flat with 2014, it remained firmly in control of the number one spot. There were, however, some significant changes in the remainder of the top 10 ranking. SK Hynix continued its ascent up the semiconductor company rankings that started a few years ago and moved into 5th place in 1Q15, displacing Micron. With Qualcomm’s sales hitting a soft patch and SK Hynix continuing to gain share in the memory market, IC Insights believes that the company could move past Qualcomm into the fourth spot when the full-year sales totals for this year are tallied. While MediaTek’s growth has slowed somewhat from its torrid pace over the past few years, the company posted a year-on-year sales increase of 12% to move into the top 10.

IC Insights believes that MediaTek will remain in this position in the full year 2015 ranking. Although Sharp as a whole is having a difficult time, its semiconductor group, which represents only about 14% of the company’s corporate sales, posted a whopping 62% growth rate, the best 1Q15 sales increase of any top-20 semiconductor supplier. This sales surge was almost entirely due to the company’s success in the CMOS image sensor market. As would be expected, given the possible acquisitions and mergers that could occur this year (e.g., NXP/Freescale, GlobalFoundries/IBM’s IC group, etc.), as well as any new ones that may develop, the top 20 semiconductor ranking is likely to undergo a tremendous amount of upheaval over the next couple of years as the semiconductor industry continues along its path to maturity.

Product Spotlight

APV1111GVY

Panasonic

Panasonic PhotoMOS® Photovoltaic MOSFET High-Power Drivers

| SKU: | |

|---|---|

| Stock: | 3490 |

| Cost: | $3.95 |