The top 10 semiconductor R&D spenders in 2015

Semiconductor industry spending on R&D grew by just 0.5% in 2015, which was the smallest increase since the 2009 downturn year and significantly below the CAGR of 4.0% in R&D expenditures during the last 10 years, according to IC Insights’ 2016 edition of The McClean Report. The 0.5% increase nudged worldwide R&D spending by semiconductor companies to a new record-high level of $56.4bn in 2015 from the previous peak of $54.1bn in 2014, says IC Insights’ flagship market analysis and forecast report on the IC industry.

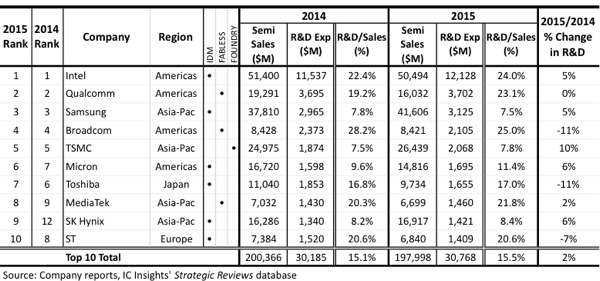

Growing concerns about the weak global economy, slumping sales in the second half of the year and unprecedented industry consolidation through a huge wave of merger and acquisition agreements weighed on semiconductor R&D spending in 2015. The 2016 McClean Report shows Intel continuing to lead all semiconductor companies in R&D spending in 2015, accounting for 22% of the industry’s total research and development expenditures. The top 10 R&D ranking is shown in Figure 1.

Following Intel in the 2015 R&D ranking are Qualcomm, Samsung, Broadcom and TSMC, the world’s largest wafer foundry. The top five spenders were unchanged from 2014, but below that point, the rankings of most companies were shuffled. Micron Technology moved up to sixth in 2015, swapping positions with Toshiba, which fell to seventh in the new ranking. MediaTek went from ninth in 2014 to eighth place, while SK Hynix climbed from 12th to ninth in 2015. ST slid from eighth in 2014 to 10th in 2015 and Nvidia fell out of the top 10 to 11th place in 2015.

Figure 1 - top 10 semiconductor R&D spenders

The top 10 in the R&D ranking collectively increased spending on research and development in 2015 by about 2% compared to the 0.5% increase for total semiconductor R&D expenditures in the year. Combined R&D spending by the top 10 exceeded total expenditures by the rest of the semiconductor companies (about $30.8bn versus $25.6bn) in 2015 - something that has continued to hold true since 2005 and probably well before that, according to The 2016 McClean Report.

Intel’s R&D expenditures grew 5% in 2015, which is significantly below its 13% average increase in spending per year since 2010 and slightly under its 8% annual growth rate since 2001, the new report says. Underscoring the growing cost of developing new IC technologies, Intel’s R&D-to-sales ratio has climbed significantly over the past 20 years. In 2010, Intel’s R&D intensity level was 16.4% of revenue spent in research and development compared to 24.0% in 2015. Intel’s R&D-to-sales ratios were 14.5% in 2005, 16.0% in 2000 and just 9.3% in 1995.

With worldwide semiconductor sales falling nearly 1% in 2015 to $353.6bn and R&D spending rising 0.5% to $56.4bn, the industry’s R&D-to-sales ratio grew slightly to 16.0% from 15.8% in 2014. Since 2000, the semiconductor industry’s annual R&D-to-revenue ratio has average 16.0%. The McClean Report forecasts semiconductor R&D spending to grow about 4% in 2016 $58.9bn and reach $76.3bn in 2020, which would represent a CAGR of 6.7% from 2015. By between 2016 and 2020, the semiconductor industry’s R&D-to-revenue ratio is expected to average 16.4% compared to 16.2% from 2011 to 2015.

Product Spotlight

APV1111GVY

Panasonic

Panasonic PhotoMOS® Photovoltaic MOSFET High-Power Drivers

| SKU: | |

|---|---|

| Stock: | 3490 |

| Cost: | $3.95 |