Medical systems drive semiconductor sales

According to IC Insights’ IC Market Drivers report, smaller and more powerful medical systems are driving up sales of ICs, sensors and other devices for the medical semiconductor market. IC Insights believes medical semiconductor sales growth will strengthen this year and next before sliding back in the next expected economic slowdown in 2017 (see image below).

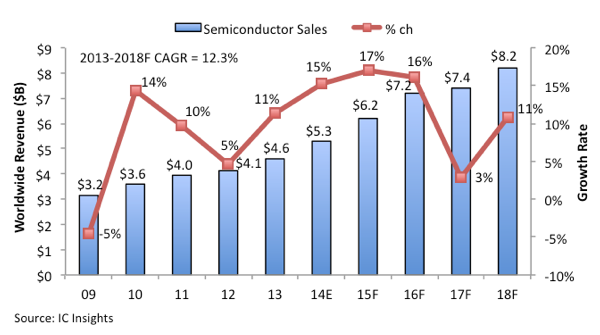

Between 2013 and 2018, worldwide medical semiconductor sales are projected to rise by a CAGR of 12.3%, reaching $8.2bn in the final year of the forecast. In the 2008-2013 period (which included the 2009 downturn), medical semiconductor sales grew by a CAGR of 6.9%.

The IC portion of the medical semiconductor business is expected to rise by a CAGR of 10.7% to $6.6bn in 2018 while the marketshare for optoelectronics, sensors/actuators and discretes is forecast to grow by an annual rate of 20.3% to $1.6bn that year (primarily due to strong demand for solid-state sensors and optical imaging devices).

Medical semiconductor market forecast

ICs and other semiconductor technologies continue to play key roles in reshaping and redefining medical systems. With more medical imaging systems being digitised and healthcare equipment running under computer control, IC-driven advancements are happening almost as quickly as they are in mobile phones and many consumer electronics. Government certification can slow some system introductions. The scaling of IC feature sizes, SoC designs, improvements in sensors and powerful AFE data converters are reducing the size of medical diagnostic equipment and the cost of using them.

Developments of new medical systems for imaging, diagnostics, treatment and surgery are heading in two different directions as equipment makers respond to growing pressures for lower costs and increased availability of healthcare worldwide. In one direction, new medical equipment is becoming smaller and less expensive so that systems can be used in the rooms of hospital patients, clinics and doctor offices. These systems cost 10-25% of the price of large diagnostic equipment such as traditional MRI and CT scanners, which can cost $1m and are normally installed in medical-imaging centres or in dedicated hospital examination rooms.

Lower-cost wearable medical systems and fitness monitors, which can wirelessly transmit vital signs and other readings to doctors or be used as 'activity trackers' for health-conscious individuals, are seeing tremendous growth. In some cases, medical and fitness-monitoring applications can be performed directly by smartphones using their embedded sensors and downloaded software apps. However, medically certified mobile healthcare devices are usually required in most countries for monitoring patients and the elderly in their homes. The information is sent to doctors via wireless connections to mobile phones or the internet.

The second major trend in medical equipment is the development of more powerful and integrated systems, which are expensive but promise to lower healthcare costs by detecting cancer and diseases sooner and supporting less invasive surgery for quick recovery times and shorter stays in hospitals. Computer-assisted surgery systems, surgical robots and operating-room automation are among new technologies being pursued by some hospitals in developed markets.

High growth in lower-cost systems along with the rising price tag of more sophisticated hospital equipment in developed country markets is expected to increase total medical electronics systems sales by a CAGR of 8.2% between 2013 and 2018, to $70.1bn in the final year of the forecast.

Product Spotlight

APV1111GVY

Panasonic

Panasonic PhotoMOS® Photovoltaic MOSFET High-Power Drivers

| SKU: | |

|---|---|

| Stock: | 3490 |

| Cost: | $3.95 |