China’s final chance to achieve its IC industry ambitions

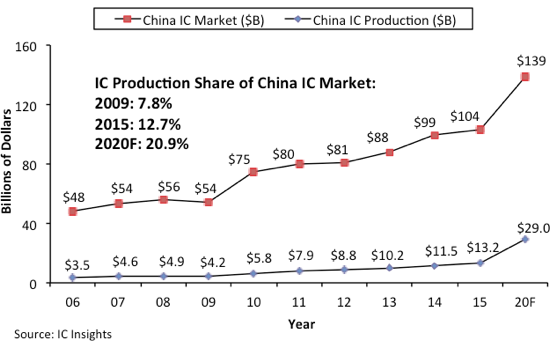

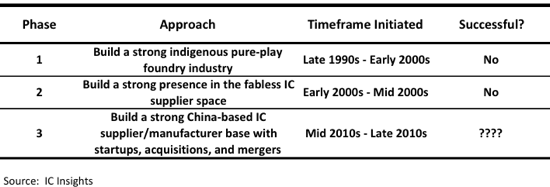

Over the past 20 years, China has become increasingly frustrated over the gap between its IC imports and indigenous IC production (Figure 1). It has often been quoted over the last couple of years that China’s imports of semiconductors exceeds that of oil. In its upcoming Mid-Year Update to The McClean Report 2016 (released at the end of this week), IC Insights examines the “Three-Phase” history of China’s attempt at strengthening its position in the IC industry that started in earnest in the late 1990s (Figure 2).

Figure 1 - China IC market vs. China IC production trends

In the late 1990s China began to contemplate ways to grow its indigenous IC industry and assisted in creating Hua Hong NEC, which was founded in 1997 as a joint venture between Shanghai Hua Hong and Japan-based NEC (it merged with Grace in 2011). Then, as part of the country’s 10th Five Year Plan (2000-2005), establishing a strong China-based IC foundry industry became a priority. As a result, pure play foundries SMIC and Grace (now Hua Hong Semiconductor) were both founded in 2000 and XMC was founded in 2006. This effort is categorised by IC Insights as Phase 1 of China’s IC industry strategy.

Figure 2 - The three phases of China's IC industry strategy

In the early 2000s, to help boost the sales of its indigenous foundries, as well as ride the strong wave of fabless IC supplier growth, the Chinese government began attempts to foster a positive environment for the creation of Chinese fabless companies. It should be noted that eight of the current top 10 Chinese fabless IC suppliers were started between 2001 and 2004 and seven of them were in the top 50 worldwide ranking of fabless IC companies last year. This stage of China’s IC industry strategy is labelled by IC Insights as Phase 2.

IC Insights believes that Phase 3 of China’s attempt at creating a strong China-based IC industry began in 2014, just before the start of its 13th Five Year Plan which runs from 2015 through 2020. As discussed in detail in the Mid-Year Update, this Phase is being supported by a huge “war chest” of cash that is intended to be used to purchase IC companies and their associated intellectual property, provide additional funding to China’s existing IC producers (e.g., SMIC, Grace, XMC, etc.), and to help establish new IC producers (e.g., Sino King Technology, Fujian Jin Hua, etc.).

In 1Q16, the U.S. Department of Commerce slapped an export ban on U.S. IC suppliers’ shipments of ICs to China-based telecomms giant ZTE in response to the company allegedly shipping telecommunications equipment to Iran while it was under trade sanctions by the U.S. This ban, if fully enacted, would have a devastating effect on ZTE’s telecomms equipment sales (including mobile phones). Thus far, the export ban has been postponed until 30th August, 2016 pending further investigation by the U.S. Department of Commerce.

The situation regarding ZTE and the abrupt announcement earlier this year of export controls on the company by the U.S. government sent shock waves throughout the Chinese government as well as China’s electronic system manufacturers. At this point in time, such potentially drastic measures taken by the U.S. government against such a large Chinese electronics company has bolstered the Chinese government’s resolve to make China more self-sufficient regarding IC component production, spurring increased emphasis on “Phase Three.”

Further trends and analysis relating to China and worldwide IC market forecasts through 2020 are covered in the 250-plus-page Mid-Year Update to the 2016 edition of The McClean Report.

Product Spotlight

APV1111GVY

Panasonic

Panasonic PhotoMOS® Photovoltaic MOSFET High-Power Drivers

| SKU: | |

|---|---|

| Stock: | 3490 |

| Cost: | $3.95 |